Comments Off on Business Line of Credit: What It Is, How It Works & When to Use It

What Is a Business Line of Credit and How Does It Work?

Every small business goes through phases of growth, slow seasons, and unexpected expenses. To stay financially steady during these shifts, many business owners rely on a business line of credit — a flexible financing tool designed to help manage cash flow and short-term needs. Whether you’re stocking inventory, covering payroll, or preparing for busy months, a line of credit can make all the difference.

What Is a Small Business Line of Credit?

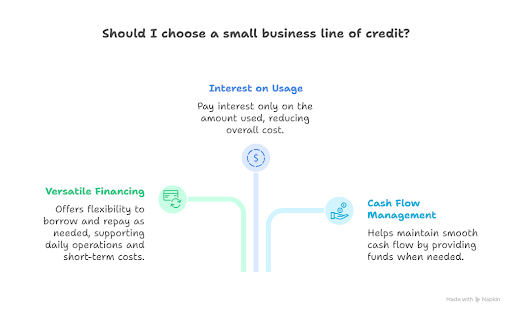

A small business line of credit is a revolving credit account that lets you borrow funds whenever your business needs them — up to a approved limit. It works much like a credit card:

You draw only what you need You pay interest only on the amount you use As you repay, your available credit refreshes

This makes a line of credit for small business a highly versatile financing option and different from a traditional business line of credit loan, where you receive a lump sum upfront and repay it over time.

Businesses often choose this financing because it helps support everyday operations, handle short-term costs, and maintain smooth cash flow.

How Does a Business Line of Credit Work?

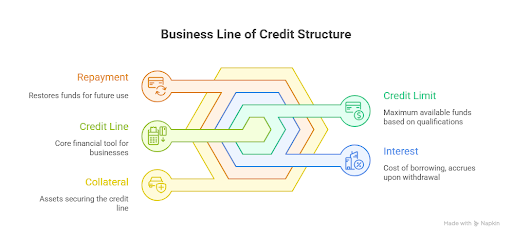

Once you are approved, your lender assigns a credit limit — for example, $10,000, $50,000, or more depending on qualifications. You can use this limit to cover any business-related expense such as:

Purchasing inventory Paying for supplies Meeting payroll Managing seasonal slowdowns Funding small growth initiatives

Interest starts accumulating only when funds are withdrawn. As you repay the borrowed amount, those funds become available again, giving your business ongoing access to working capital.

For many owners, this revolving structure makes a credit line for business more practical than a traditional commercial loan.

Secured vs. Unsecured Business Line of Credit

A secured line of credit requires collateral — such as equipment, vehicles, or business assets. These usually offer higher limits and lower commercial line of credit rates.

An unsecured business line of credit, on the other hand, doesn’t require collateral. Instead, lenders evaluate your business credit history, financial stability, and revenue. These lines offer flexibility but may have slightly higher rates depending on the lender.

Both types help businesses gain access to working capital, whether for routine expenses or unexpected financial needs.

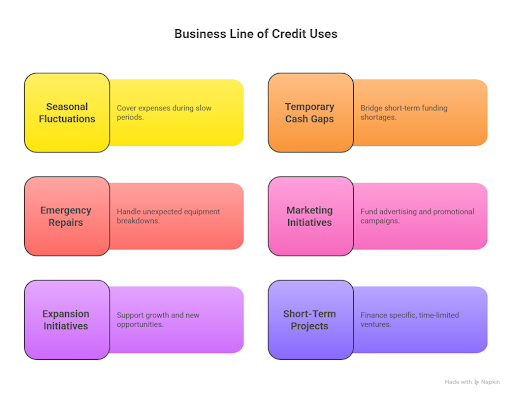

Common Uses of a Line of Credit for Business

Businesses often rely on lines of credit for business in situations such as:

Unlike loans designated for specific purchases, a business line of credits can be used for almost any operational expense. Many businesses even use it alongside their bank accounts through checks, online transfers, or mobile banking tools.

Business Line of Credit Requirements

Lenders have different criteria, but most will look at:

Time in business (commonly 1–2 years) Annual revenue Business credit score Financial statements (bank statements, tax returns, P&L) Outstanding debts

If you’re applying for a bank business line of credit, expect a more detailed review compared to online lenders — but often with more favorable terms.

Rate Considerations

Compared to credit cards, which may charge 20%+ APR, a business line of credit typically offers lower interest rates. However, rates depend on:

Whether it’s secured or unsecured Your credit profile Your lender (banks tend to offer the best rates)

Businesses with strong credit histories may qualify for the most competitive commercial line of credit offers.

Benefits of Maintaining a Business Line of Credit

Keeping a line of credit business account in good standing can help your business:

Strengthen its credit score Qualify for higher limits in the future Build a positive borrowing history Access better financing options later

Many business advisors recommend starting with a modest limit, using it responsibly, and repaying quickly — a strategy that reinforces your financial reliability.

Is a Business Line of Credit Right for Your Company?

If your business needs ongoing access to flexible funding or faces seasonal swings, a business line of credit may be one of the best tools to keep operations smooth. It’s ideal for short-term expenses, unexpected costs, and working capital shortages — helping your business grow at its own pace.